Australia’s latest CPI data points to a more complex inflation environment for general insurers. Headline inflation has eased slightly, but underlying inflation remains above the Reserve Bank’s target band, while cost pressures in areas directly relevant to home and motor claims continue to build. We explore what the May CPI release means for insurers, with three areas to watch across claims costs, pricing assumptions and household affordability.

Headline inflation over the 12 months to May 2026 was 4%, down from 4.2% over the 12 months to April 2026. However, trimmed mean inflation* – the Reserve Bank’s preferred measure of underlying inflation – increased by 0.2% over the month to 3.6%, persisting above the 2-3% target band.

There are a variety of both compounding and offsetting effects flowing through the economy. Fuel/energy costs have increased due to the Iran war, inducing flow-on impacts to other sectors of the economy through increased freight and agricultural costs. Recent policy effects including the fuel excise subsidy and other cost-of-living measures by State and Federal governments have also been influential market forces.

What insights can insurers take from the May CPI release? Here are our top three highlights.

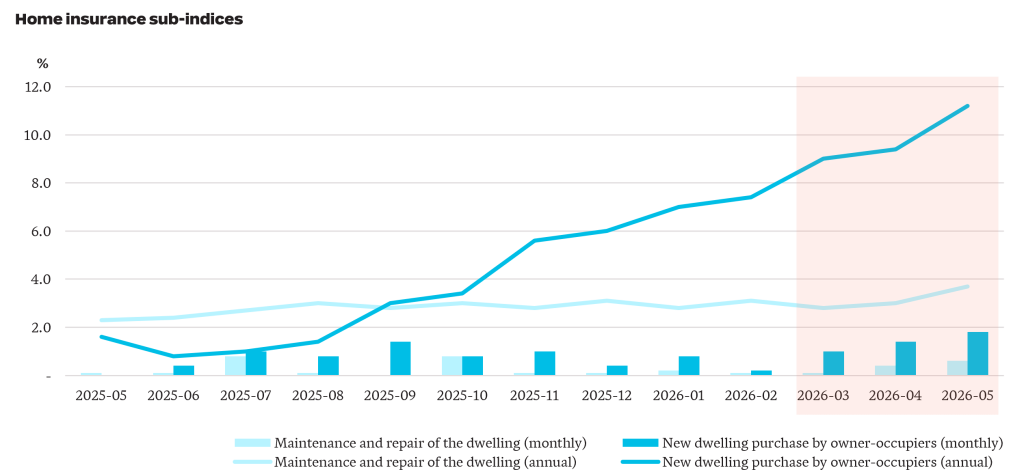

1. New dwelling costs increased by 11% over the year to May, up from 2% over the year prior. Maintenance and repair cost increases have been more subdued, increasing by 4% over the year to May, up from 2% over the year prior.

The new dwelling purchase series (blue series) includes changes in building materials costs and labour costs. This index has increased steadily from November 2025, outpacing the increase in maintenance and repair costs (light blue series). The double digit increase in new dwelling costs aligns with increased competition for skilled tradespeople and construction materials, with greater demand continuing to push prices higher.

There are early signs effects from the conflict in the Middle East is flowing through to higher new dwelling costs, as seen in the shaded orange region in the chart. Inflation over the months of April 2026 and May 2026 was 1.4% and 1.8%, respectively. This compares with 1.2% and 0% over the same months last year. Month-to-month inflation figures are volatile and are to be treated with caution.

As maintenance and repair costs and the cost of new dwellings are subject to different inflationary pressures, insurers will need to closely monitor the mix between partial and total losses.

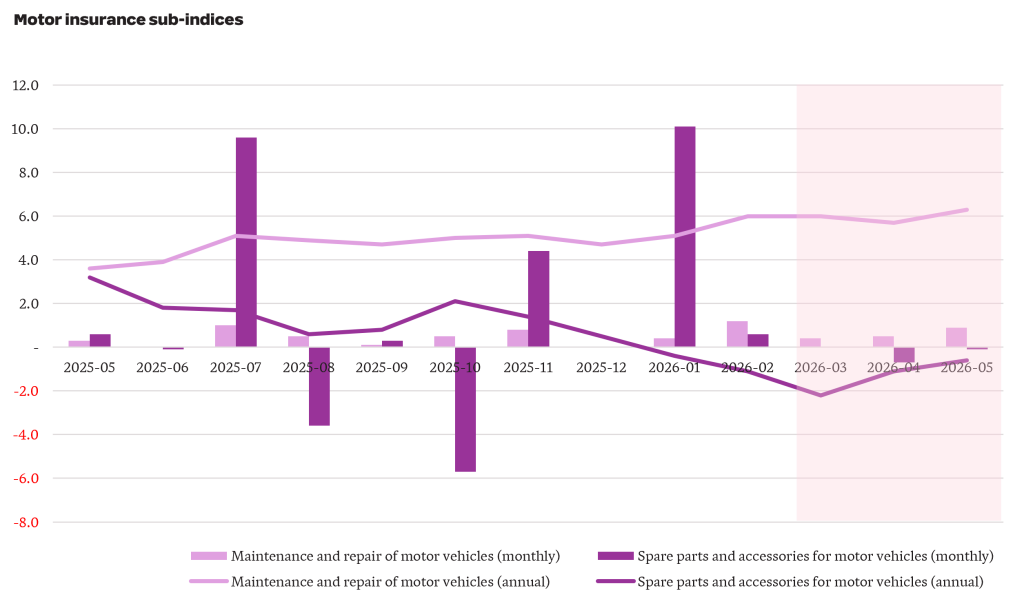

2. The cost of maintaining and repairing motor vehicles has increased by 6% over the last year, up from 4% the year earlier.

The cost of maintaining and repairing a motor vehicle (light purple series) has grown faster than the broader CPI and has increased through FY26. This series captures the cost of labour, parts and materials, with the increase over the year attributable to both rising labour costs and vehicle complexity. Over the same period, the cost of spare parts and accessories (dark purple series) has declined by 0.6%.

Motor insurers should be cognisant of growing labour and repair complexity costs which have outstripped general inflation. We expect this trend to persist as electric vehicle penetration continues to accelerate (see our recent article on EVs for more details), requiring more specialised skillsets and parts.

3. Consumers are continuing to feel the squeeze. Since the start of 2024, prices as measured by the CPI have increased by 11% to the end of March 2026. Meanwhile, wages, as measured by Average Weekly Earnings, have only increased by 8% meaning that real wages have declined by 3% over the period.

This is only part of the picture. May CPI data shows the cost of non-discretionary items has increased faster than discretionary items. Non-discretionary items are goods and services which are purchased to meet a basic need – for example, food, shelter and healthcare. Discretionary items are those which are considered “optional”, such as takeaway meals, alcohol and holidays. The chart below highlights non-discretionary inflation has been persistently higher than discretionary inflation over FY26 and consequently, is also higher than headline CPI inflation.

Increases in the cost of non-discretionary items have a larger impact on lower-income households as these essentials cannot be easily deferred or substituted as household budgets tighten. Following the Middle East conflict, non-discretionary inflation has spiked up to the 5%, driven by increases in automotive fuel prices. As a result, low income households are facing more pressure than implied by the headline inflation numbers.

Cost of living has been of substantial focus in recent years, particularly politically where the government has introduced measures to offset part of the impact of rising prices. For example, the Fair Work Commission’s decision to increase the National Minimum Wage by 6% is expected to go part way to addressing some of these pressures for the lowest paid workers.

What do the latest numbers mean for the insurance industry?

- The pressure on affordability is intensifying. Broader cost of living pressures, combined with higher-than-average levels of inflation in home and motor repair costs which will increase premiums, will squeeze already-tight household budgets.

- As the status of the conflict in the Middle East changes regularly, so too do inflation expectations. We are only now starting to see the impacts of higher fuel prices flow through to the cost of materials. Even if the conflict ends tomorrow, expectations are that it will take over six months for things to return to normal. This will have implications for pricing and reserving.

- Financial vulnerability is expected to increase and will impact renewal rates, selected excesses and sums insured.

The May CPI release reinforces that insurers are operating in an environment where inflationary pressure is uneven, volatile and closely tied to household affordability. For insurers, the challenge is not only to respond to current inflation, but to track how these pressures flow through portfolios over time and adjust pricing, reserving and risk settings as new trends emerge. Additionally, insurers will need to closely monitor the impact of affordability pressures on their portfolios so their products align with customer needs to maintain relevance, trust and resilience.

*The trimmed mean removes the most extreme price movements.